SpaceX IPO Aftermath: $2.1T, Grok, and Cursor

So, it actually happened.

On June 12, 2026, Elon Musk did what many thought he’d never do: he took SpaceX public. Trading under the ticker symbol SPCX on the Nasdaq, the stock debuted at a fixed IPO price of $135 per share, raising a historic $75 billion.

By the closing bell on day one, shares had surged to $161.11, pushing the market cap to a staggering $2.1 trillion. For a brief moment on June 16, euphoria drove the stock to an all-time high of $225.64, valuing the company at over $2.6 trillion and briefly surpassing Amazon. Since then, gravity has kicked in, settling SPCX around $180 as of today.

But as the dust settled, analysts and retail investors alike began digging into the prospectus. And let me tell you, what is written inside that document absolutely sent me lol!

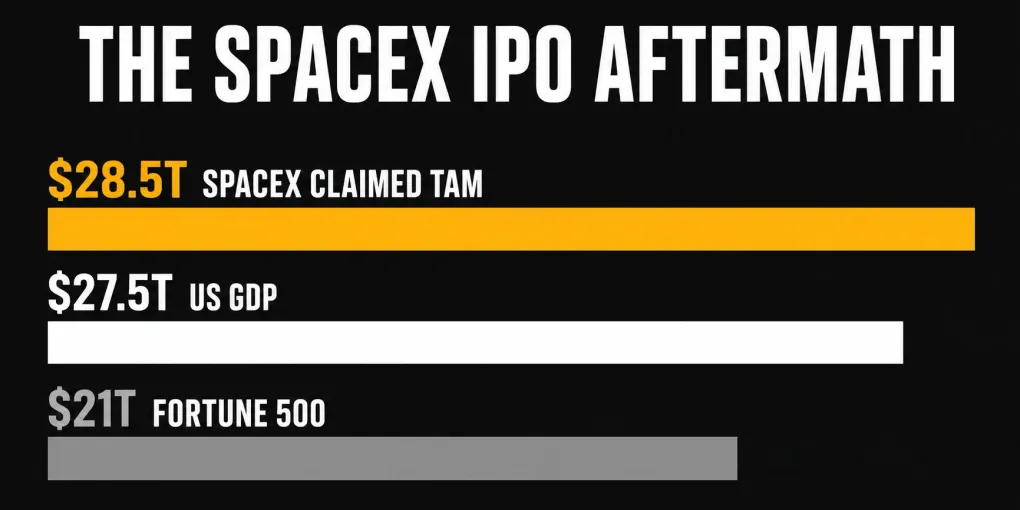

The $28.5 Trillion TAM Elephant in the Room

According to the IPO prospectus, SpaceX’s Potential Addressable Market is a whopping $28.5 Trillion.

Just to give you some context, this number is roughly equal to the yearly nominal GDP of China, India, and France combined. Better yet, the combined revenue of all US Fortune 500 companies is around $21 Trillion. So yeah, SpaceX’s claimed TAM is larger than the Fortune 500 revenue combined. Totally normal stuff.

To understand how they got here, we have to look at the merger with xAI earlier this year. By combining the rocket business, the Starlink constellation, and Elon’s AI venture, the company pitched itself as a single integrated space-connectivity-intelligence platform.

Here is how the prospectus breaks down that $28.5 Trillion TAM:

Visualizing the Scale: SpaceX TAM vs. Reality

The Internal Breakdown of SpaceX's TAM

Looking at the chart, the disconnect is immediate. The core rocket launch business—which SpaceX spent two decades perfecting and dominates globally—is valued at a TAM of “only” $370 billion. Starlink’s global connectivity TAM is listed at $1.6 trillion.

The remaining $26.5 Trillion? Entirely attributed to Artificial Intelligence.

The Mechanical Index Squeeze (The 4% Float Trap)

If you’re wondering how a company with such wildly speculative numbers could surge 67% in its first four days of trading, you have to look past the rocket emojis and look at the market mechanics. The post-IPO price action was not driven by fundamental equity research; it was a textbook example of a synthetic supply squeeze.

When SpaceX went public, it structured the offering with an incredibly small public float. Only about 4% to 5% of the company’s total shares were made available for public trading. That means that while the company was valued at $1.77 trillion at pricing, only about $75 billion worth of stock was actually floating in the open market.

This is where index-inclusion mechanics turned the listing into a powder keg:

- CRSP and FTSE Russell Fast-Track: Earlier in 2026, index providers adjusted their rules to fast-track massive tech listings. SpaceX was added to CRSP and FTSE Russell indices on June 18—its fifth trading day.

- The Passive Scramble: Passive index funds tracking these benchmarks are legally mandated to hold SpaceX stock in exact proportion to its market capitalization. Analysts estimated that this forced index-tracking funds to purchase between $10 billion and $16 billion worth of SPCX shares in a matter of days.

- The Nasdaq-100 Clock: The Nasdaq-100 is set to include SPCX within 15 trading days of listing, triggering another wave of forced buying.

- S&P 500 Lockout: The only index holding back is the S&P 500. S&P Global maintained its strict eligibility rules requiring four cumulative quarters of positive GAAP earnings and a 12-month waiting period, locking SpaceX out for now.

When passive managers are forced to buy billions worth of a stock with virtually zero open-market supply, price discovery goes out the window. The index-inclusion pump created a mechanical bid, driving shares to the $225 peak. It was not about whether the company was worth $2.6 trillion. It was about passive funds being forced to buy at whatever price was on the screen.

The xAI Premium and the Robot Dilemma

This brings us to a crucial point about the $28.5 trillion TAM: the numbers rest on assumptions about AI that are questionable in themselves.

I mean, until and unless AI replaces the entire global workforce, how do you even get to a $26.5 trillion addressable market? And if you think about it the other way: if no one is working and everything is done by AI, then who exactly is paying money to these companies? The robots? 😭

But even if we accept that optimistic macro assumption, I’m not quite sure how much xAI will realistically be able to capture from this AI market. According to the prospectus, most of the future AI revenue is supposed to come from enterprise applications. And in my personal experience, Grok isn’t even in the top 3 for enterprise AI right now.

Currently, Anthropic is leading enterprise AI, even ahead of OpenAI. Then there’s Google Gemini, and some very capable open-source models like DeepSeek and Kimi.

Grok’s share sits at 3rd place in the US chatbot market at 17.8%, but that is mostly driven by X app integration and social media usage, not enterprise adoption. Enterprise buyers care about brand reputation, political neutrality, and data privacy. Translating consumer engagement on social media into a multi-trillion-dollar enterprise business is a massive stretch.

The $60 Billion Dilution Bombshell: Why Did SpaceX Buy Cursor?

But the real post-IPO shock came just days after the listing. On June 15, SpaceX announced it had exercised its option to acquire Anysphere, the startup behind the popular AI coding editor Cursor, in an all-stock deal valued at a staggering $60 billion.

Naturally, public market investors who had just bought into the IPO were left asking: Why did SpaceX buy Cursor?

To understand this, you have to look at the deal’s structural mechanics. SpaceX had secured a contract option in April 2026 that allowed them to either acquire Cursor for $60 billion or enter a commercial partnership for $10 billion. Fresh off the IPO, Elon decided to exercise the acquisition option, utilizing the public stock as M&A currency.

By structuring the deal during the height of the index-inclusion pump, SpaceX was able to use its highly inflated stock price as arbitrage. The final number of shares printed for Cursor’s founders and backers is determined by a 7-day volume-weighted average price (VWAP) around the transaction date. Because the stock was mechanically squeezed to $225, SpaceX printed fewer shares to hit the $60 billion valuation, reducing the nominal share dilution on paper.

However, the transaction structure remains highly risky. The merger agreement includes a $10 billion termination fee if SpaceX backs out, and a $4 billion break fee if the deal is blocked by antitrust regulators. If regulators flag the combination of a launch monopoly, a satellite internet monopoly, and a dominant AI coding platform as anticompetitive, public shareholders are on the hook for billions.

Furthermore, it establishes a worrying corporate governance precedent. It shows that public markets are being utilized as an endless printing press to fund Elon’s broader AI land grab, diluting launch and satellite investors to buy pre-revenue software startups.

Morningstar’s Valuation Gravity: Is SpaceX Stock SPCX Overvalued?

Following the listing, major research firms began issuing their verdicts, and they weren’t all starry-eyed. Morningstar released a scathing note initiating coverage on SPCX with a fair value estimate of just $62 per share—suggesting the stock was trading at a nearly 200% premium at its peak.

This has sparked intense debate: is the stock overvalued?

According to the bear case, the underlying business is incredibly capital-intensive. Launch services and Starlink require billions in ongoing CapEx. And now, they are combined with xAI, which is posting massive operating losses as it chases compute power.

In fact, reports of a potential $20 billion bond offering are already circulating, just weeks after raising $75 billion in the IPO. Why? Because building orbital data centers, launching hundreds of Starlink V3 satellites, and securing GPU clusters is a black hole for cash.

The cash flows from the highly profitable launch and satellite businesses are being completely consumed by xAI’s computing research and development.

The launch of SPCX options trading on June 17 has finally given short-sellers a tool to express their skepticism, which is why we saw the quick correction from the $225 peak to $180 as the initial index-buying frenzy subsided.

IMO…

SpaceX is a generational company. Starlink is a natural monopoly, and Starship will dominate launch logistics for the next decade. But at a $1.8 Trillion valuation, you aren’t buying a launch company — you are buying a speculative AI narrative wrapped in a rocket booster.

For retail investors, the opportunity cost of holding SPCX at these valuations is high, especially with immediate dilution from acquisitions like Cursor and massive capital requirements looming.

Which sector do you think is next in line for a bull run? Drop it in the comments, I would love to hear your thoughts.

Pankaj, signing off. See you next time! ☕